Q2 2021 Investment Commentary

by Boston Trust Walden

July 12, 2021

Financial Markets

Stocks, and financial assets generally, continued to move higher during the second quarter. As the US began emerging from the pandemic in earnest, domestic large capitalization stocks, as measured by the S&P 500, rose another 8.6%. Year-to-date returns for the Index now stand at over 15%. Smaller capitalization stocks, as well as most primary international stock indices gained during the quarter, too. Bond prices also rose as the yield on the 10-year US Treasury dropped by over 0.25% to finish the quarter at 1.47%. Interest rates play a prominent role in the valuations investors place on stocks, with valuations often rising as interest rates decline. This is especially true of companies that are expected to achieve above-average growth or have profit streams at some point in the future (oftentimes solely in the distant future). Accordingly, the decline in longer-term interest rates likely contributed to faster growing, but often currently less profitable, companies leading the market. Growth stocks outperformed value stocks by over six percentage points during the quarter, as measured by the Russell 1000® Growth and Russell 1000® Value indices, though the performance of the latter remains ahead year-to-date.

Investment Perspectives

The results of an impressive, albeit uneven, domestic vaccination program are evident in lower COVID-19 infection rates. With health risks diminishing, Americans are eagerly leaving their homes to re-engage with their communities and make up for lost time. This includes a resumption in spending that was put off during the pandemic, and indeed the economic recovery is progressing quicker—and stronger—than expected. GDP expanded at a 6.4% annualized rate in the first quarter and is expected to have gained more steam in the second quarter. The same is true for the path of corporate earnings – the primary driver of long-term stock returns. Wall Street analysts have not only forecasted this year’s corporate profits to surpass their pre-pandemic (i.e. 2019) levels, but their expectations for profit growth have continued to rise as the economic recovery has come into focus. At the beginning of the year, analyst consensus called for aggregate 2021 S&P 500 earnings to be 10% higher than those in 2019. Just six months later, analysts now expect aggregate profit growth of more than 25% vs. 2019 results (if achieved, this would represent a 55% improvement from the depressed earnings of 2020). Double digit profit growth is expected to continue into 2022.

Sources: FactSet, Standard & Poor’s

Inflation: Passing Through or Here to Stay?

Inflation is a natural byproduct of economic resurgence. In any expansionary period, strong demand can push prices higher before supply has an opportunity to catch up. We are seeing that in spades with exploding demand meeting supply chains that are still coping with pandemic-induced disruptions. Combine those elements with the depressed baseline of lower prices last year (due to then-collapsing demand), and it is hardly surprising that in the last several months the prices of many goods and services have risen at paces not seen for multiple decades. We expect elevated readings to continue for some time, but we do not view them as indicative of an entrenched long-term trend. Rather, we believe that the secular forces that have kept inflation at moderate levels over the last several decades are likely to persist. These disinflationary factors include the continued effects of global manufacturing, trade, and capital flows, as well as persistent technological advancements. Based on the action of bond yields during the quarter, which fell rather than rose (as is more typical during times of heightened inflationary fears), the market seems to be dispelling longer-term inflation concerns, too.

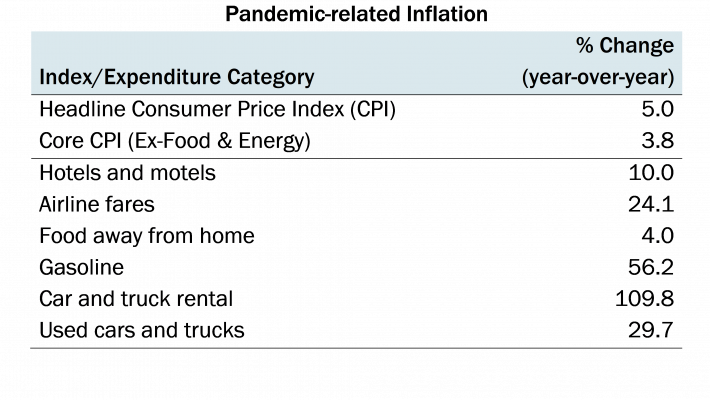

The media often focuses on aggregate inflation rates like the Consumer Price Index (CPI) or the Core CPI (which excludes food and energy). However, May’s Core CPI 3.8% year-over-year increase only tells part of the story as the markets in certain underlying goods and services better illustrate the current dynamics of the economy. A case in point are prices for used cars and trucks, which jumped an eye-popping 30% from a year ago. In fact, given the magnitude of the increase and their significance in the CPI basket, used cars and trucks accounted for roughly a full percentage point of the total 3.8% increase. Like many aspects of the economy, the causes of such a dramatic price change in one market is the result of shifts in the markets for other goods and services.

In the throes of the pandemic last spring, travel largely came to a standstill. Rental car companies were faced with a choice: Let their fleets languish in their lots and lose value, or sell them for cash to help manage a severe downturn in their businesses. They chose the latter en masse and sold significant portions of their fleets. Despite the influx of supply, used car prices held firm as US consumers, both wary of mass transit during the pandemic and sporting stimulus payments and/or accumulated savings, readily bought them up. Consumers were also stepping up their purchases of new cars, electronic devices, household appliances, and other goods that drastically increased demand for microchips at a time the global semiconductor industry was confronting pandemic-related and other supply disruptions. The result was, and continues to be, a global chip shortage. This is impacting new vehicle production and has prevented rental car companies from replenishing their fleets to meet the currently exploding demand. Indeed, the supply/demand imbalance has contributed to rental car prices skyrocketing—up 110% year-over-year in May, including double digit increases for the last several months. Accordingly, rental car companies are holding onto the cars in their fleets, depriving the used car market from an important supply source and driving up prices. These types of interrelated issues are notable given the significant upheaval in prices, but we expect them to moderate as supply chains continue to normalize.

Source: US Bureau of Labor Statistics (May Report)

Slow Hiring and Stable Wages

Though the consumer economy is roaring back to life, the employment picture has been slower to return to pre-pandemic levels. While any hiring process takes more time than the swipe of a credit card, the labor market has some unique hurdles. First, the speed at which demand returned is likely to have caught some employers flat-footed in being appropriately staffed. Now that they are hiring in earnest, it has been a challenge to find willing workers.

There are many possible headwinds to more rapid employment gains. Parents may be holding off until schools are fully back in session, while other potential job seekers might be waiting for further vaccination adoption or more clarity on the risks of COVID variants. Others may be waiting for their accumulated savings, bolstered by stimulus payments, to wind down before pursuing additional income. But perhaps contributing most obviously to this reticence are the expanded and enhanced unemployment benefits provided by the Federal government. These measures were a critical lifeline to millions when major swaths of the economy came to a virtual standstill almost overnight. They were generous enough that in some cases, people earned more by not working. Though states are increasingly opting out of these programs that are set to expire in September, it’s unsurprising that they would be a headwind for employers looking to hire without substantially increasing wages. Indeed, according to the New York Fed’s surveys, the average lowest wage a non-college educated worker would be willing to accept in a new job has increased by almost 20%—to over $61,000—since before the pandemic.

In aggregate, employers appear to be holding the line on wages despite the impediment to hiring. Average hourly earnings for private, non-farm workers have only risen modestly in recent reports. Importantly, wage increases have been at levels below those of recent inflation readings—a key rationale for our expectation of moderating prices. Should wages begin to rise more rapidly, it could be cause for greater concern. However, even then we are not resigned to an entrenched trend. The Federal Reserve has the policy tools to tamp down on an overheating economy and intensifying inflation. Even public comments from the Fed can serve to temper inflationary expectations, helping to quell anticipatory price increases before they accelerate.

Outlook and Positioning

We expect the economic recovery to remain strong through the remainder of this year and well into 2022. The US consumer has demonstrated its resilience and we expect spending to remain strong, thereby supporting the continued rebound in corporate profits and providing a healthy backdrop for stocks. Though price increases are part and parcel of any expansion, we expect that current elevated inflation will abate as shorter-term factors resolve.

Risks remain, however. Asset prices are inextricably linked with today’s low interest rate environment. This includes stocks and bonds, whose price movements have become increasingly correlated, as well as real estate and most other assets. Accordingly, the prospect of quickly rising rates, via policy error or otherwise, does present a latent risk for financial assets. Other risks are evident as well. A resurgence of COVID-19 and its variants, either domestically or globally, could interrupt the economic recovery and investor confidence. Though geopolitical risks are always apparent in some form, the increasing spate of cyberattacks targeting critical infrastructure is particularly notable given their potential to disrupt economic progress.

We continue to view equities favorably relative to bonds. The S&P 500’s aggregate valuation of 22x current year earnings estimates is above historical averages. Still, it is not unreasonable given the low interest rate environment; expected returns for stocks remain materially higher than those implied by yields on investment grade fixed income instruments. Though the latter remain useful for portfolio stabilization and cash flow needs in concert with client-specific considerations, we expect stocks to drive returns in multi-asset portfolios. As always, we are focused on identifying companies with sustainable business models and strong financials. We are also attentive to those companies that will participate in the economic recovery yet are not included among the pockets of the market trading at valuations that imply an unsustainable level of future growth. Looking out further, we do not expect more fiscal relief packages related to the pandemic, but additional government spending could help to extend the economic expansion. Though only in the early innings of negotiation, we will continue to track progress and the details of infrastructure bills making their way through Washington.

Boston Trust Walden Company is a Massachusetts-chartered bank and trust company.

Past performance is not indicative of future results.

Data Sources: FactSet, Standard & Poor’s, US Bureau of Labor Statistics, Federal Reserve Bank of New York

The information presented should not be considered as an offer, investment advice, or a recommendation to buy or sell any particular security. The information presented has been prepared from sources and data we believe to be reliable, but we make no guarantee to its adequacy, accuracy, timeliness or completeness. Opinions expressed herein are subject to change without notice or obligation to update.

About Boston Trust Walden Company

We are an independent, employee-owned firm providing investment management services to institutional investors and private wealth clients.