Q4 2021 Investment Commentary

by Boston Trust Walden

January 12, 2022

Financial Markets

Stocks, as measured by the S&P 500 Index, finished the year in fabulous fashion. The Index returned 11.0% during the fourth quarter, bringing full year gains to 28.7%. Remarkably, the cumulative return over the past three years is now over 100%. Equity returns in 2021 were led by US large capitalization growth stocks, though gains were still substantial in other segments of the market, too. Smaller domestic companies, as measured by the Russell 2000® Index, gained 14.8% during the year. Most developed international equity markets also registered significant gains, but the MSCI Emerging Markets Index was in the red. The latter was dragged down by the poor performance of China’s equity market, which comprises roughly a third of the Index.

Interest rates rose across all maturities – pushing the primary broad bond market index returns into negative territory for the year. The yield on the 10-year Treasury bond rose by 0.58 percentage points during 2021, closing the year at 1.51%. Among other assets, rising demand caused economically sensitive commodities to gain ground. Crude oil prices surpassed pre-pandemic levels, while copper prices reached all-time highs during the year.

Investment Perspectives

What a difference a year makes. Though yet another sharp wave of COVID-19 infections means the two-year anniversary of the pandemic is all but certain to be marked with continued anxiety and disruption to our daily lives, in aggregate, we are in a far better position than we were a year ago. We now have multiple tools to manage the virus’s spread and its impacts. First and foremost is a collection of vaccines that are being distributed with relative success, including over 500 million doses domestically and close to 9 billion globally. Going further, evolving testing technology, monoclonal antibody treatments, antiviral pills, as well as increasing knowledge about the virus’s biology have aided the tireless efforts of healthcare workers and public health experts. These virus-related developments factored heavily into the economic recovery of the past year and have significant influence on its continuation.

US economic and business fortunes improved dramatically over the course of 2021 with a resurgence in economic activity. Once full year data is tallied, real US GDP is expected to have expanded by close to 6%, with aggregate S&P 500 corporate profits growing by over 50%. Though these figures are measured against 2020’s recessed levels, they also exceed previous high-water marks. Real GDP is 2% higher, and corporate profits 25% higher, than 2019. Today’s primary economic risks, including a reduction of monetary and fiscal policy support, sustained inflation, and elevated equity valuations, are largely byproducts of positive developments associated with the recovery and expectations for continued growth.

Full Employment

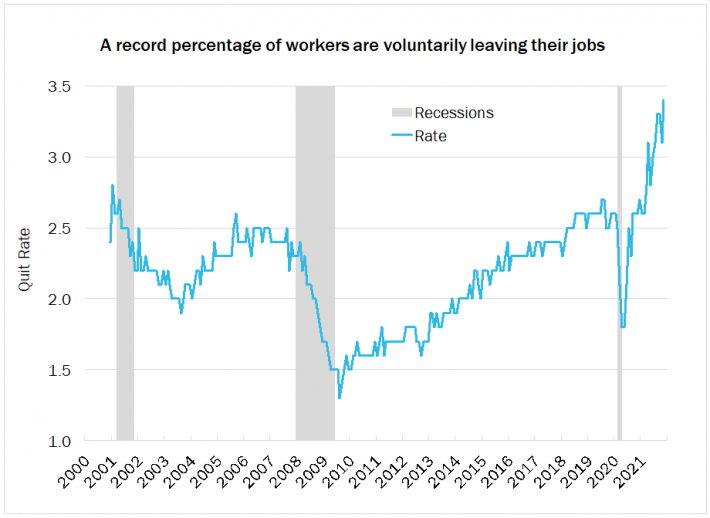

The labor market has run in tandem with the economy’s resurgence. At year-end 2020, the unemployment rate was down significantly from its pandemic highs, but still elevated at 6.7%. Now the headline rate is approaching “full employment” levels, coming in at 3.9% in December. The strength of the economy is evidenced by the tight job market, which has enabled a shift of power to workers. This includes substantially higher wages (particularly for lower paid workers, as we noted in our commentary last quarter), multiple high profile strikes and labor union activities, as well as a record high “quit rate,” or the percentage of total employed that are leaving their jobs voluntarily. The latter includes individuals seeking new jobs that may offer better pay and/or working conditions, and others that may be leaving the workforce entirely. Indeed, the participation rate, the working age population that are either employed or seeking employment, has fallen by 1.5 percentage points since the end of 2019 to 61.9%. However, those permanently leaving the workforce have disproportionately been older workers that likely feel more secure in retirement due to higher 401(k) balances and home property values. Likewise, those staying in the job market are exhibiting economic confidence with a willingness to risk the security of their current job to seek a better opportunity. As employers have sought to both retain staff and attract new workers, wages have risen. Those higher wage levels are likely here to stay, as it is far more difficult to lower rather than raise compensation. While growing paychecks helps workers and their budgets, the potential of an extended cycle of wage hikes adds to wider inflation concerns.

Source: Federal Reserve Bank of St. Louis. Quit rate as percent of total monthly private payrolls, seasonally adjusted.

Strong Demand, Higher Prices

Secure employment and higher wages, along with savings bolstered by stimulus checks and rising asset values, have led to strong aggregate consumer demand. But given continued activity constraints related to the pandemic, spending patterns have, at least temporarily, shifted to favor physical goods over services. Unfortunately, supply chains for many goods are still reeling from pandemic-related disruptions, including abrupt shutdowns, loss of workers, and border closures. Consequently, shortages and/or long lead times for seemingly everything – from raw materials to critical components and finished goods – are rampant. Though there have been some flickers of progress, getting the gears of global supply chains humming again has taken more time than hoped. And with no signs of demand abating, the bottlenecks are unlikely to be substantially resolved until we are well into 2022. Aside from consumers’ frustration, the supply-demand imbalance has left businesses struggling to maintain, let alone build, ample inventories. Though this limited supply provides a governor on near-term sales, a forthcoming build-up of inventories has the potential of feeding continued economic activity after some of the heightened demand for goods normalizes.

With outsized consumer demand, continued supply shortages, and rapidly rising material and wage costs, it is unsurprising that prices have risen. Indeed, we have seen elevated inflation readings since the late Spring, when vaccination rates ramped up, cases came down, and the economy sprung back to life. Year-over-year increases of the headline Consumer Price Index (CPI) have been at or above 5% since May – reflective of current dynamics as well as the depressed comparison periods from the prior year. It is worth reemphasizing, however, that this current bout of inflation is inextricably linked with economic expansion. This sharply contrasts with the run of elevated inflation in the late 1970s. That period of ‘stagflation’ was marked by shocks on the supply side without the robust demand and economic production we are seeing today. Regardless, a protracted inflationary period remains a risk if expectations for the same initiate a cycle of anticipatory price and wage increases. Such dynamics would be destructive to real economic growth as well as profit margins of those corporations who do not wield pricing power – both of which could have negative consequences for stocks.

Waning Policy Support

Once again, all eyes are on the Federal Reserve. However, in contrast to earlier this year when the Fed was taking extraordinary measures to stimulate growth like it had during most of the pandemic, the central bank is now seeking to prevent inflation from becoming a more serious problem. Jerome Powell, recently renominated for another term as Fed Chairman, has decidedly changed his tune. He has admitted that pricing pressures have and will go on for longer than originally expected, though he still expects elevated inflation to be temporary. With underlying growth on firm footing, the central bank has begun tapering its longer-term bond purchases and telegraphing its plans for future short-term interest rate increases. The shift in Fed rhetoric was not the death knell for financial markets some investors may have feared. In fact, subsequent to public comments regarding the Fed’s plans, stocks continued to rise and longer-term interest rates moved lower.

Like the above monetary matters, political winds also shifted substantially in the past year. The Democrats’ victories in the run-offs for Georgia’s Senate seats last January resulted in a razor thin majority and the ability to pass the American Rescue Plan last March – a $1.9 trillion stimulus bill that helped fuel this year’s economic recovery. More recently, President Biden signed the bipartisan Infrastructure Investment and Jobs Act into law in November. The law’s $550 billion of new Federal funding can further buttress the current economic expansion, while the underlying investments in transportation systems, bridges, high-speed internet, and the like may reduce frictions in the economy for decades to come. Further fiscal support for consumers may be forthcoming if Democrats can resolve their intra-party differences to pass their Build Back Better bill without GOP support. Even if they can do so, it is worth recognizing that these two packages will almost certainly represent a material reduction in spending versus the unprecedented fiscal relief provided by Congress in 2020 and early 2021. That the expenditures are longer-term in nature, however, could be constructive towards lengthening the expansion.

Outlook and Positioning

Though many conditions have improved over the last year, some issues are enduring. Indeed, as we turn the page to 2022, the pandemic remains in the forefront. While new variants continue to pose a risk, vaccines and treatments have, so far, been effective at allowing continued normalization within our society and the economy. In line with long-term trends, corporate profit growth can continue to fuel additional gains for stocks. Though we do not expect earnings to expand at the same torrid pace of 2021, we enter 2022 with consensus forecasts of S&P 500 earnings growth at 9% — a very healthy level. At the same time, expectations for rising interest rates reduce already-low expected returns for fixed income instruments. We should note, however, that rapidly rising rates would likely negatively impact most financial assets, including stocks. Geopolitical risks, including China’s evolving economic policies, heightened fears of a Russian invasion of Ukraine, and a number of national elections around the globe (including US mid-terms), provide opportunities for other unanticipated outcomes. Though bonds can serve as a portfolio stabilizer in such times of market volatility, we continue to favor equities in the context of client-specific guidelines due to their more attractive long-term expected returns.

Though the Fed has begun its efforts to tamp down on pricing pressures (while leaving the expansionary cycle intact), we remain cognizant of the risks associated with entrenched inflation expectations and rising interest rates. These economic risks provide greater impetus for our fundamental research focus on sustainable business models. This includes substantiating that portfolio companies have the requisite pricing power to pass on rising input costs and maintain profit margins, as well as the financial strength to tolerate higher borrowing costs. As always, but especially in light of substantial increases in stock values, we are also attuned to avoiding companies that have unreasonable expectations of future growth embedded in their share prices. Thus, we remain focused on constructing portfolios that consist of high quality companies with reasonable valuations.

Boston Trust Walden Company is a Massachusetts-chartered bank and trust company. Past performance is not indicative of future results. Data Sources: FactSet, Federal Reserve Bank of St. Louis, US Bureau of Labor Statistics. The information presented should not be considered as an offer, investment advice, or a recommendation to buy or sell any particular security. The information presented has been prepared from sources and data we believe to be reliable, but we make no guarantee to its adequacy, accuracy, timeliness or completeness. Opinions expressed herein are subject to change without notice or obligation to update.

About Boston Trust Walden Company

We are an independent, employee-owned firm providing investment management services to institutional investors and private wealth clients.